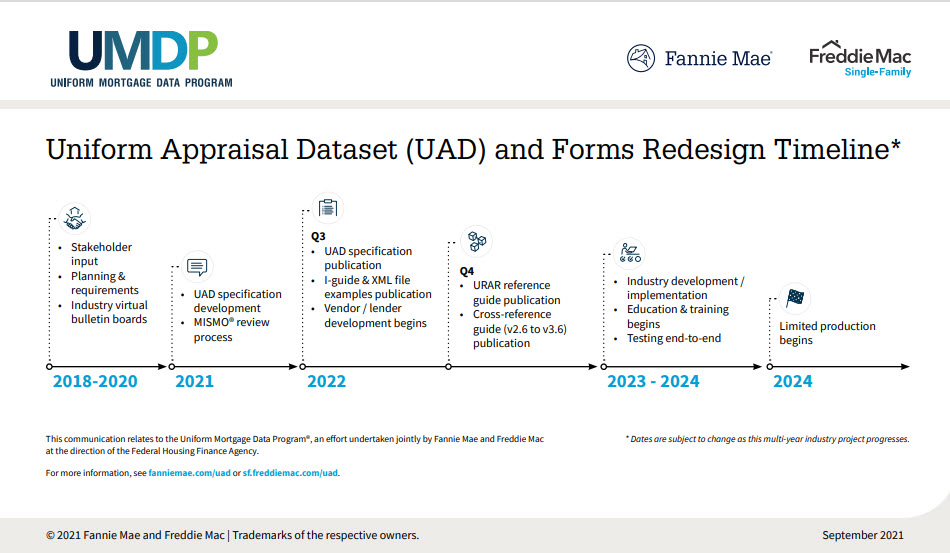

With the new URLA behind us…along comes the next major change in residential lending. Fannie Mae and Freddie Mac (aka the GSEs) have provided an update on the new URAR. Yes, the Uniform Residential Appraisal Report is undergoing some major changes. Here are just a few highlights: Input was gathered from 107 stakeholders across the industry in designing the new form. The key benefits of the new form are: Dynamic output with commentary placed within each …