The mortgage origination field can seem incredibly appealing, offering the potential for high earnings, autonomy, and the satisfaction of assisting others with their home financing. However, this allure often leads to unrealistic expectations and, ultimately, early disillusionment. To avoid these common pitfalls, newcomers must prioritize ongoing mortgage loan originator professional development right from day one. The Reality Behind Industry Promises True success in the mortgage industry requires setting realistic goals and taking full ownership of …

I have been receiving many inquiries about what it takes to start a mortgage broker business and how to get started. I recently spoke to a gentleman who thought he wanted to start his own business, but after our lengthy conversation, he came to the conclusion “I just want to originate.” How much time and money did a conversation possibly save him? In 1994, I became an originator. I was being recruited by a local …

For the past 20 years, I have been teaching real estate classes. Initially, I began teaching as a strategic piece of my mortgage loan originator professional development. I was looking for a way to build and maintain professional relationships and gain referrals. Unlike sponsoring open houses or arranging casual coffee meet-ups, I found that educating was a far more effective and respectable approach. The courses I taught were not just general marketing or time management …

The definition of insanity: doing the same things over and over and expecting different results. Welcome to the mortgage business! Mortgage company owners and recruiters often entice new Mortgage Loan Originators (MLOs) into the industry with the allure of minimal entry requirements. However, this approach frequently leads to a puzzling outcome: these eager new entrants struggle to succeed because they lack continuous mortgage loan originator professional development. The Missing Link in MLO Success The critical …

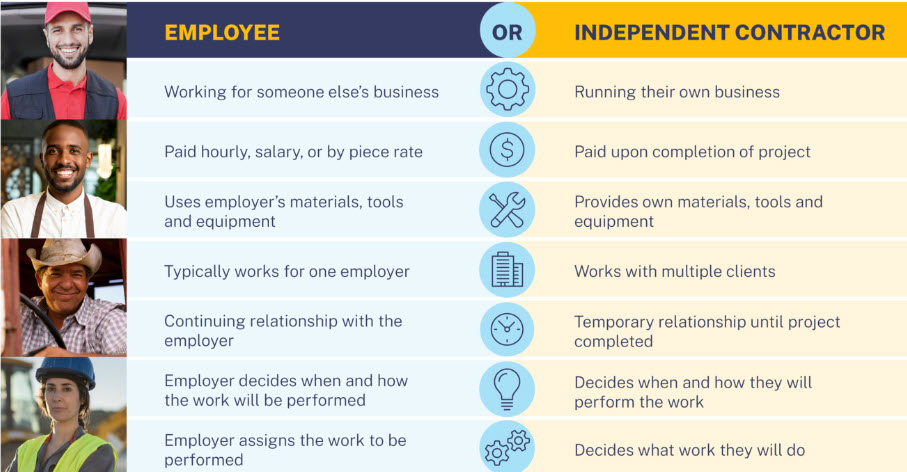

On October 13, 2022 the Federal Department of Labor published findings in Vol. 87, No. 197 of the Federal Register. The W-2/1099 controversary hits many businesses. As stated in previous posts, there is no special 1099 consideration for mortgage loan originators. Regardless of which state you work in or which type of employer your work for, Mortgage Loan Originators are required to have their income reported on IRS Form W-2. There are many companies that …