The Myths and Realities -1099 vs W-2 for Loan Originators!

As someone who has followed this topic for many years, with many debates, I’ve heard it all. Just today, posts on Facebook brought it up…again! What’s different now is a few weeks ago, I decided to get reliable information from a reliable source.

To help clear up the confusion, I am sharing below some of what I have known and some of what I have learned.

State and federal governments rely on revenue to function. One significant long-term impact of COVID-19 has been the sharp increase in federal debt due to extensive stimulus spending. Meanwhile, state and local governments faced tough challenges in balancing budgets without raising taxes or cutting essential services. Payroll taxes and unemployment insurance remain critical sources of revenue, and with a growing emphasis on fair treatment of workers, equity, and equality, worker rights—particularly their paychecks—are under greater scrutiny. To address the trillions of dollars in budget gaps at both federal and state levels, new revenue streams will need to be tapped. If worker classification becomes a potential source of revenue, it’s worth preparing for changes ahead!

So, let’s start at the beginning.

The IRS and Departments of Labor (DOL) (Federal and State) start with the presumption that ALL workers are “employees” until they prove they meet the Independent Contractor status, a burden which mortgage loan originators cannot meet.

“But they are outside salespeople!” “They work independently!” “I don’t tell them when to work!” “They are remote!”

Oh…the justifications! Consider the following:

Under Federal law, sponsoring “employers” know, or should know, they are responsible for oversight of their employees. Likewise, sponsored “employees” know, or should know, they cannot originate mortgage loans without an employer who holds an active entity (broker or lender) license. And…they are only permitted to be sponsored by one sponsor at a time. And…that sponsoring employer exerts control over hiring, firing, compensation, training, systems, vendor management, processing, security, compliance, underwriting, closing and funding. And… how can “independence” even hold up, when companies pay for MLO licensing, education and testing to recruit new employees? Imagine your plumber asking for you to pay for his license and C.E.?

So here’s the core question nobody seems to address:

If MLOs are truly independent contractors, why do they need a company sponsorship?

- Most employers understand the rules; many try to skirt them. Justifying independent status is usually a weak argument.

- Employees themselves try to justify it for personal or tax reasons.

Why is this topic still a question? Where does this confusion come from? Let’s look at some myths…

” I am an independent contractor because I am strictly commissioned.” This argument was presented to me years ago by one of my “employees.”

- This argument fails because how a person’s income is calculated is a completely separate issue from how the wages are reported to the IRS.

- It is not what the employer or employee want that matters, it is how the law defines the job.

“My employer and I agreed that I will get a 1099!”

- You can agree to whatever you want, but that won’t stand up in an IRS or state audit. Even if it’s written in your “EMPLOYMENT” agreement that you are not an employee, it doesn’t make it so.

I am exempt from overtime because I am an “outside sales person.’

- This argument fails because an exemption for overtime pay does not change the employer/employee relationship. In fact the argument backfires, because it implies the worker is an employee by virtue of the exemption.

“But I work independently. My manager doesn’t tell me how to originate.”

- This argument fails because what a manager tells a worker doesn’t establish how the law defines the job.

- Mortgage loan originators are employees. Period. The company is responsible for the actions of the employee no matter how they agree to work.

“I was told to just set up an LLC for the payments to go to so I can deduct my business expenses.”

- This is a dicey one! So…that LLC is a NMLS licensed entity holding a valid state license? Then…WHY DO YOU NEED A SPONSOR?

- And, creating a business for the sole purpose of evading tax law is in itself a violation.

“But my state mortgage regulator says they don’t care if we report wages on 1099.”

- They’re right! They don’t care! They enforce LICENSING and INSURANCE laws. The IRS doesn’t care about the SAFE Act either!

Recently, I had the opportunity to get some clarity from someone who worked for the Federal Department of Labor for 33 years and who kindly provided me with some references that I thought might be helpful to pass on. Actually…hold that thought!

Before we get to labor law, hour and wage law, the FHA and IRS rules…let’s start with something we should all be familiar with; The SAFE Act.

Section 1007.104 – Federal Register Policies and Procedures —

Covered financial institutions that have one or more MLO employees must adopt and follow written policies and procedures to carry out their SAFE Act responsibilities. This applies to all covered financial institutions that employ individual MLOs, where MLOs act within the scope of their employment.

Additionally, covered financial institutions must conduct annual independent compliance tests to ensure compliance with the regulation. The policies and procedures must be appropriate to the nature, size, complexity, and scope of the institution’s mortgage lending activities and apply only to those employees acting within the scope of their employment at the institution. The policies and procedures must:

- Establish a process for identifying which employees must be registered;

- Require MLOs be informed of the registration requirements of the SAFE Act and instructed on how to comply;

- Establish procedures to comply with the SAFE Act regulation’s unique identifier requirements;

- Establish reasonable procedures for confirming adequacy and accuracy of MLO employee registrations…

- Establish reasonable procedures and tracking systems for monitoring compliance for registration and renewal

- Provide for annual independent testing for SAFE compliance by institution personnel or an outside party;

- Provide for appropriate action if employees fail to comply with the SAFE Act or the institution’s related policies and procedures…and other appropriate disciplinary actions;

- Establish a process for reviewing employee criminal history and taking appropriate action

- Establish procedures that ensure that any 3rd party with which the institution has arrangements related to mortgage loan origination has policies and procedures to comply with the SAFE Act and SAFE Act regulation, including appropriate licensing and/or registration of individuals acting as MLOs.

If that’s not enough…let’s look at a few highlights from the FHA:

https://www.hud.gov/sites/documents/SFH_FAQ_PREVIEW.PDF

“The lender must require its employees to be its employees exclusively, unless the lender has determined that the employee’s other outside employment, including any self-employment, does not create a prohibited conflict of interest…”

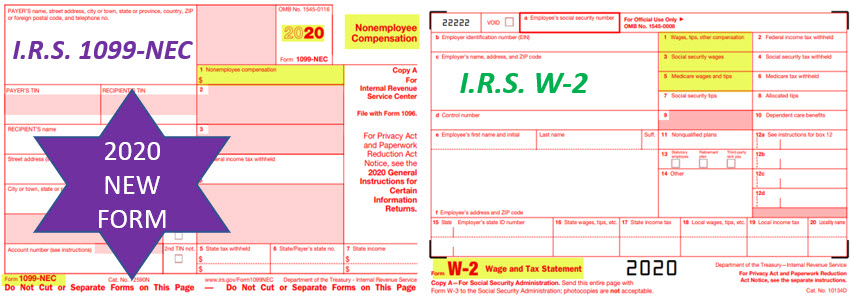

“The lender must compensate employees on a salary, salary plus commission, or commission only. The lender may pay bonuses with any of these three compensation plans. The lender must report all employee compensation on IRS Form W-2.

“Can FHA Approved Lenders use nonemployees as Loan Officers? “No.” The lender may only use contract support for administrative and clerical functions.

Besides, can you really make an argument that, for FHA loans, the worker is a W-2 employee, but for NON-FHA loans, they are independent contractors? It’s the same job with the same employer.

Now let’s see what Federal Department of Labor and IRS have to say:

First, the March 2010 Administrator’s Interpretation No 2010-1. Before you click the link, bear one thing in mind.

The entire subject of whether MLOs are exempt from overtime is predicated off the accepted notion that we are talking about W-2 Employees. I don’t know of a true “independent contractor” who gets overtime! “Hi, Mrs. Homeowner. I am the contractor who repaired your deck. The quote I provided needs to be increased because I worked on the deck for 42 hours last week and I will need time and a half for the extra two hours!”

Second is the DOL 7 point test that all MLOs cannot get past.

- The extent to which the services rendered are an integral part of the principal’s business.

- The permanency of the relationship.

- The amount of the alleged contractor’s investment in facilities and equipment.

- The nature and degree of control by the principal.

- The alleged contractor’s opportunities for profit and loss.

- The amount of initiative, judgment, or foresight in open market competition.

- The degree of independent business organization and operation.

So let’s take the above one at a time.

- Are the services being provided by the worker different from the services of the business they are providing them for? Originators are in the same business as their employer, which is very different from the bookkeeper who does work for a mortgage company or the marketing firm that puts ads together for the mortgage company.

- Isn’t the goal of a hiring company to recruit, hire and RETAIN the employees that prove valuable to the organization? How many MLOs are offered a “three-month stint” working for a mortgage company? Do employment agreements have an end date?

- While MLOs look for companies to pay for their licensing and training, they certainly aren’t forking over any money to invest in the business. If they are, that’s a different story than the one we are addressing.

- There are mortgage companies who claim MLOs “work independently” and that’s fine. However, if the proverbial stuff hits the fan, the EMPLOYER is on the hook for the actions of the MLO. They cannot be separated, as federal and state laws require the employer to “oversee” what MLOs do and the results of their work. And who’s responsible for compliance?

- Most MLOs have never been told, “hey, we had a tough month, we need you to put up some money for the losses we incurred.” Nor, in most instances, do they share in the profits of the business.

- Initiative, judgment and foresight…most MLOs are not paid to determine how the business should compete. An originator who determines their personal marketing strategy does not remove the employee status.

- Most MLOs have no control over the organization and operation of the company. They do not set terms with vendors; likewise they do not set up LLCs, partnerships or corporations, and decide on tax strategies. They don’t hire CPAs and attorneys. They do not normally recruit or hire closers, underwriters, funders or business operations staff such as accounting, marketing and compliance.

Add that list to the IRS list of requirements to meet the independent contractor status to better determine how to properly classify a worker, and consider these three categories – Behavioral Control, Financial Control, and Relationship of the Parties.

Behavioral Control: A worker is an employee when the business has the right to direct and control the work performed by the worker, even if that right is not exercised. Behavioral control categories are:

- Type of instructions given, such as when and where to work, what tools to use or where to purchase supplies and services. Receiving the types of instructions in these examples may indicate a worker is an employee.

- Degree of instruction, more detailed instructions may indicate that the worker is an employee. Less detailed instructions reflect less control, indicating that the worker is more likely an independent contractor.

- Evaluation systems to measure the details of how the work is done points to an employee. Evaluation systems measuring just the end result point to either an independent contractor or an employee.

- Training a worker on how to do the job — or periodic or on-going training about procedures and methods — is strong evidence that the worker is an employee. Independent contractors ordinarily use their own methods.

Financial Control: Does the business have a right to direct or control the financial and business aspects of the worker’s job? Consider:

- Significant investment in the equipment the worker uses in working for someone else.

- Unreimbursed expenses, independent contractors are more likely to incur unreimbursed expenses than employees.

- Opportunity for profit or loss is often an indicator of an independent contractor.

- Services available to the market. Independent contractors are generally free to seek out business opportunities.

- Method of payment. An employee is generally guaranteed a regular wage amount for an hourly, weekly, or other period of time even when supplemented by a commission. However, independent contractors are most often paid for the job by a flat fee.

Relationship: The type of relationship depends upon how the worker and business perceive their interaction with one another. This includes:

- Written contracts which describe the relationship the parties intend to create. Although, a contract stating the worker is an employee or an independent contractor is not sufficient to determine the worker’s status.

- Benefits. Businesses providing employee-type benefits, such as insurance, a pension plan, vacation pay or sick pay have employees. Businesses generally do not grant these benefits to independent contractors.

- The permanency of the relationship is important. An expectation that the relationship will continue indefinitely, rather than for a specific project or period, is generally seen as evidence that the intent was to create an employer-employee relationship.

- Services provided which are a key activity of the business. The extent to which services performed by the worker are seen as a key aspect of the regular business of the company.

The take away from my conversation with the DOL veteran was that “no one criteria will make or break the status determination. All jobs must be looked at in total.” What does the complete job circumstance really look like? That is how enforcement is handled.

Generally, the IRS oversees FEDERAL tax enforcement and the State DOLs oversee state tax enforcement. Like any other regulation, the more restrictive laws trump the less restrictive ones.

As an example, last year the New Jersey Department of Labor (NJDOL) issued rules and guidance, as well as penalties, for misclassification of employees. This year, they clarified and basically doubled down by announcing that misclassification is just one issue. They also determined that employees being misclassified for the purpose of avoiding insurance benefits is insurance fraud! And they gave themselves a nice easy way to enforce it.

- “This law opens avenues to the NJDOL that never existed previously. Rather than pursue enforcement …the NJDOL can file a public lawsuit seeking immediate injunctive relief to shut down offending businesses and seek fees and costs in the process.

- A5892/S3922 makes it a violation of the New Jersey Insurance Fraud Prevention Act to “make a false or misleading statement, representation or submission, including failing to properly classify employees in violation of state wage, benefit and tax laws,” or to misclassify workers for purposes of evading the full payment of insurance benefits or insurance premiums. Penalties for such violations range from $5,000 for the first violation to $15,000 for the third and subsequent violations.

Virginia has a slightly different way of dealing with the issue. According to Virginia statute § 40.1-28.7:7. Misclassification of workers:

An individual, who has not been properly classified as an employee, may bring a civil action for damages against his employer for failing to properly classify the employee if the employer had knowledge of the individual’s misclassification. An individual’s representative may bring the action on behalf of the individual.

My purpose in gathering all this information is to get violators, or would be violators, to understand that the regulatory landscape may be changing. And if everyone reported wages compliantly, it would level the playing field for recruiting and hiring.

The GREAT news is, if you really have a question and want to follow the law, you don’t need to guess.

The IRS makes it easy! By filing Form SS8, there is no more guessing, rationalizing or justifying. It’s called the Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding.

If this topic is of interest, look at how one state (CA) dealt with it in the Dynamex case. Feel free to view our video episodes.

I would love to hear your thoughts: deb@cloes.online

Cloes.online 866-256-3766

You may also like

Navigating NMLS Licensing: A Step-by-Step Success Guide