The Perfect Storm: Why the Biggest Opportunity in Mortgage Origination is Right Now

The Perfect Storm: Why the Biggest Opportunity in Mortgage Origination is Right Now

Let’s be brutally honest about the last three years in the mortgage industry. With interest rates hovering at their highest levels in decades, we’ve seen a massive shrinkage in loan originations. It has been a painful period of margin compression and stalled pipelines. We’ve watched seasoned professionals leave the business out of sheer frustration, and new hires? They’ve been at an absolute, record low.

If you’re looking from the outside in, you might think the mortgage business is dead. But if you truly understand how this industry works—and I have spent over 35 years in this business managing over $1 billion in real estate loans—you know we are sitting on the edge of the greatest income opportunity we have seen in a very long time.

Here is the reality: the housing market is deeply cyclical. People still need to buy homes. Life events—marriages, growing families, downsizing, divorces, and relocations—do not care about the Federal Reserve’s current rate policy. That means there is massive, pent-up demand waiting on the sidelines. The moment those rates finally begin to ease and normalize, the floodgates are going to open. Millions of borrowers will be rushing back into the market to buy or refinance, and the demand for mortgages is going to skyrocket.

The Mortgage Bankers Association (MBA) is already forecasting that total single-family mortgage origination volume will increase to $2.2 trillion in 2026. The volume is coming. The only question is: who is going to capture it?

The Great Exodus: A Cleared Playing Field

Here is where it gets incredibly exciting for you. While the demand is about to surge, the supply of state-licensed Mortgage Loan Originators (MLOs) has absolutely plummeted. The mass exodus of originators over the last three years means there is far less competition. The pie is about to get much bigger, and there are significantly fewer people sitting at the table.

Let’s look at the actual data, because as an accountant, I believe the numbers tell the true story. According to industry analytics firm Ingenius, the total number of producing mortgage loan officers (those who closed at least one loan in a 12-month period) peaked at roughly 178,000 in mid-2021. By early 2024, that number plummeted by 47% to just under 94,000. Data straight from the Nationwide Multistate Licensing System (NMLS) mirrors this brutal reality, showing the number of active, state-licensed MLOs dropping from nearly 125,000 down to just over 80,000 by the end of 2023.

Nearly half of the producing loan officers in the United States have left the business. The “refi boom” order-takers who flooded the market in 2020 and 2021 couldn’t survive when the market required actual skill, relationship building, and financial acumen. They packed up and went home. What does this mean for you? It means the market has naturally culled the herd. The competition has thinned out dramatically, leaving a massive void in the market for competent, well-trained professionals to step in and take massive market share.

The Math: Uncapped Income Potential

Hope is not a strategy—math is. So let’s break down the actual income opportunity in this business when the market turns.

Unlike salaried corporate jobs with a 3% annual raise, your income in mortgage origination is tied directly to your production and your competence. While compensation models vary by company (brokerages versus banks, salary-plus versus commission-only), industry standards show that an originator typically earns a commission ranging from 0.50% to 2.50% of the total loan amount. On average, a standard commission payout is right around 1.00% to 2.00% per closed loan.

If you are working in a market with an average loan size of $500,000, and you are earning a 1% to 2% commission, that translates to a staggering $5,000 to $10,000 in gross commission for just one single closed loan.

If you commit to learning this business, mastering your craft, and building your referral pipeline with real estate agents, financial planners, and CPAs, closing 100 loans in a year is a highly achievable milestone for a dedicated professional. Let’s do the math on that. At an average of $5,000 to $10,000 per loan, closing 100 loans yields an annual income of $500,000 to $1,000,000.

Where else can you find that kind of income potential without a medical or law degree? Even if you are just starting out and you only close two loans a month in your first solid year, that is 24 loans. At $5,000 a pop, you are looking at $120,000 a year. The Bureau of Labor Statistics will tell you the “median” wage for a loan officer is around $74,000, but that includes part-timers and order-takers at local bank branches. High-volume, commission-based originators who actually know how to structure deals make multiples of that median.

Getting Started: The Path to Licensure

You can’t just stumble into making half a million dollars a year. You have to be licensed, regulated, and educated. The Secure and Fair Enforcement for Mortgage Licensing Act (SAFE Act) requires all state-licensed MLOs to pass a rigorous background process and complete specialized education.

If you are ready to enter the business, here is the exact path you need to take:

Create an NMLS Account

Your first move is to go to the Nationwide Multistate Licensing System (NMLS) website and create an account to get your unique NMLS ID number. This number will follow you for your entire career.

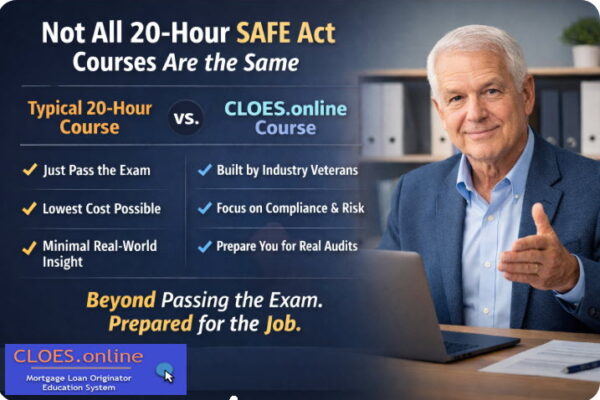

Complete the 20-Hour SAFE Act Pre-Licensing Education

You must take a 20-hour initial licensing course from an NMLS-approved provider. At CLOES.online, we offer the absolute best, instructor-led, competency-based 20-Hour courses to not only check this box but actually prepare you for the reality of lending.

Pass the National SAFE MLO Test

After your education, you must pass the National Test Component with Uniform State Content. It is a 115-question exam, and you need a 75% to pass. It is notoriously difficult, which is why taking a high-quality pre-licensing course is critical.

Complete Background and Credit Checks

You must authorize a criminal background check (CBC) and a credit report pull through the NMLS portal. Regulators want to ensure you have a history of financial responsibility before you handle other people’s money.

Sponsorship and State Licensure

Once you pass the exam and background checks, you must apply for your state license(s). Your license will become “active” once you are sponsored by a licensed mortgage employer (a broker or a lender).

Competency Over Compliance: Why Training Matters

Here is the harsh truth that most education providers won’t tell you: passing the SAFE exam is required, but it does absolutely nothing to teach you how to actually originate a mortgage.

The NMLS exam tests you on federal regulations, RESPA, TILA, and disclosure timelines. It does not teach you how to analyze a self-employed borrower’s tax returns. It does not teach you how to handle a low appraisal. It does not teach you how to structure a file so that it flies through underwriting without conditions.

If you want to be the originator making $500,000 a year, competency is expected! You cannot fake your way through complex financial transactions. That is exactly why we built our proprietary Origination Best Practices course.

This isn’t just another continuing education requirement; it is the blueprint for a successful career. Over my 28 years originating mortgages and managing a correspondent lending business, I’ve seen exactly where new originators fail. They fail because they quote rates instead of offering advice. They fail because they don’t know how to take a complete 1003 (Uniform Residential Loan Application).

Our Origination Best Practices program is a comprehensive masterclass designed to take you from a licensed novice to a confident, high-producing advisor. It covers 19 deep-dive sections, including:

- The Mystery of Appraisals: Learn how to educate consumers on valuation and save deals when the appraisal comes in short.

- Advising vs. Quoting: If you are simply quoting rates, your customer does not need you. We teach you how to analyze the market and provide strategic advice so you win the deal based on trust, not just the lowest rate.

- Reading Tax Returns: Qualifying borrowers with variable income, overtime, or self-employment requires pulling apart tax returns to find the actual “qualifying” income. This is where top originators separate themselves from the amateurs.

- Condition-less Files: We teach you the holy grail of origination—how to structure and document a loan file before submission so you don’t nickel-and-dime your borrower for documents every three days.

At CLOES.online, we don’t just want you to get licensed; we want you to thrive. We want you to be the professional in your market that realtors demand to work with because they know you close on time, every time.

The market is shifting right now. The fair-weather originators have quit. The borrowers are stacking up. The trillions of dollars in forecasted volume are coming. Now is the time to get licensed, get properly trained, and position yourself for the massive wave ahead.

You may also like

Navigating NMLS Licensing: A Step-by-Step Success Guide