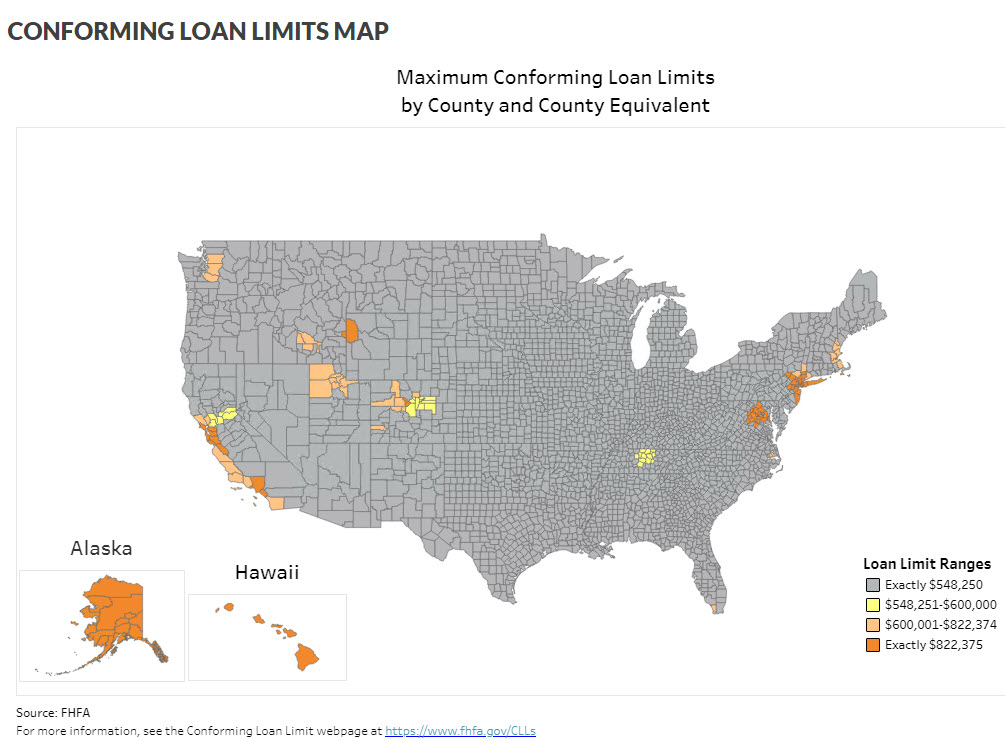

You wouldn’t know we were in the middle of a pandemic based on the housing market. That conforming limit keeps creeping up. It all seems crazy from when I started in the mortgage business in 1994, the conforming loan limit was $225,000. Fast forward 26 years…the 2020 limit was just increased another 9.0% to $548,250 for 2021. Checkout the Loan Limit Geocoder. Now, all we need to know is…what will Fannie and Freddie be doing come …