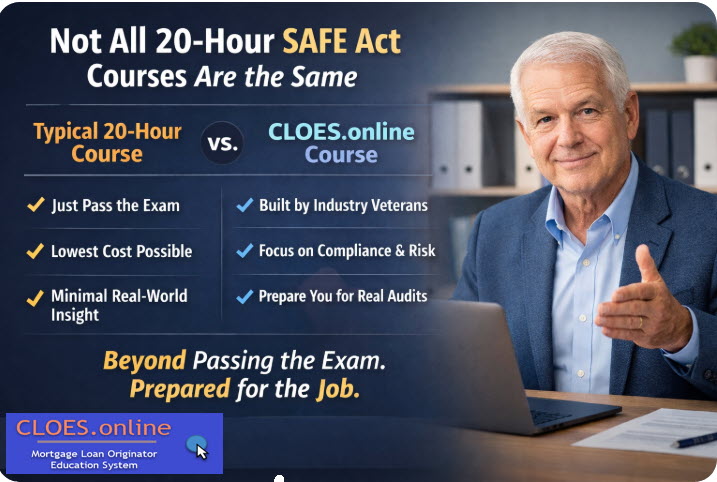

Passing the exam is required. Competency is expected. Every NMLS-approved 20-Hour SAFE Act course technically checks the same regulatory box. That does not mean they prepare you equally for the realities of mortgage lending. Most courses are built to help you pass a test. Ours is built to help you retain the content, understand your role when working with borrowers, and pass the test! Enroll Now What Most 20-Hour Courses Actually Deliver Many national providers focus …