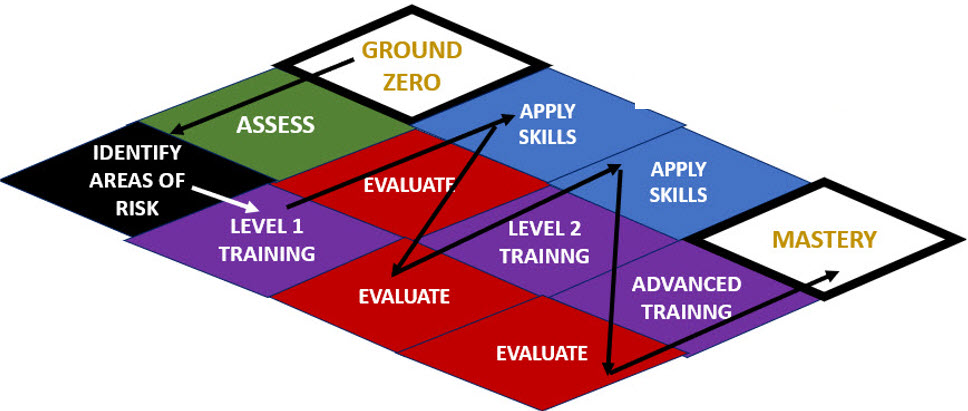

Ready to embark on a rewarding career as a mortgage loan originator? Look no further! We’re thrilled to announce our latest offering: the comprehensive 20-Hour Safe Pre-Licensing Education Program Our newest course was written by and taught by veteran mortgage loan originator Debra Killian. It’s packed with valuable insights, industry knowledge, and expert guidance and is designed to equip you with the essential skills needed to thrive in the mortgage industry. We believe that high-quality …